|

|

Post by the Scribe on Mar 29, 2020 9:19:28 GMT

|

|

|

|

Post by the Scribe on Mar 30, 2020 8:29:37 GMT

The new fed chair refused to answer the question "If the economy is so great, as it is then WHY haven't wages risen." He hemmed and hawed before saying "We don't really know." Well I know. It is called greed. It is crony capitalism. Wages will not go up unless employers are forced to raise them. Same old trickledown story republiconservatives gave us to sell their Tax reform act for the wealthy elites." Instead these corporations did stock buybacks and distributed profits to shareholders. This is why capitalism and democracy are NOT compatible.

Full interview: Federal Reserve Chair Jerome Powell

In the five months since Jerome “Jay” Powell took over as chairman of the Federal Reserve, the country is facing a growing number of tests: stagnant wage growth, tariff disputes around the world and a White House that likes to publicly offer the Fed economic advice.

In his first broadcast interview since taking the job, Powell told Kai Ryssdal that he is “not concerned” about political pressure and that he’s keeping his focus on carrying out the Fed’s mandate from Congress: “We have a long tradition here of conducting policy in a particular way, and that way is independent of all political concerns,” he said. They also talked about The White House's ongoing trade disputes, why wages aren't rising and inflation. You can also read the whole thing here.

Powell told Kai Ryssdal that he is “not concerned” about political pressure and that he’s keeping his focus on carrying out the Fed’s mandate from Congress: “We have a long tradition here of conducting policy in a particular way, and that way is independent of all political concerns,” he said. They also talked about The White House's ongoing trade disputes, why wages aren't rising and inflation. You can also read the whole thing here.

www.marketplace.org/2018/07/12/economy/powell-transcript

www.marketplace.org/popoutplayer

|

|

|

|

Post by the Scribe on Mar 30, 2020 8:30:13 GMT

Will the end of this FREE MARKET SCAM pushed by the Republiconservative Party since Reagan also spell the end of their party and the Libertarian Party? Let's hope so.

Ian Bremmer - The End Of The Free Market

Ian Bremmer - Three Choices for America's Role in the World |

|

|

|

Post by the Scribe on Mar 30, 2020 8:31:15 GMT

Deficit, debt rising in the Trump eraBy Caroline Curtin

caroline.curtin@newsday.com

Published: Thursday, April 19, 2018

The size of the federal budget deficit will rise over the next decade, in part due to recent tax and spending legislation, crossing the $1 trillion mark by 2020, according to new projections by the Congressional Budget Office.

In addition, the national debt, as measured by what is owed to the public, will nearly double, rising from $14.7 trillion in fiscal year 2017 to $28.7 trillion in 2029 according to the CBO, a nonpartisan office in Congress that produces independent analyses of budgetary and economic issues to support the Congressional budget process.

The deficit, now that the tax cut and new budget are settled

In April 2018, the CBO published revised deficit projections taking into account the new tax law and the budget and appropriations bills approved by Congress. This combination of legislation decreased the federal government’s anticipated revenue and increased estimated expenditures, which modified the CBO's deficit forecast as initially published in June 2017. It is anticipated that the federal government's outlays will continue to exceed receipts continuing a deficit trend over the next decade.

Running Deficits, Increasing Debt

The CBO's latest projections estimate that debt held by the public, which is the government's debt owed to individuals, companies, local governments, foreign entities, and Federal Reserve Banks, will continue to increase over the next decade. Current projections estimate that the debt will rise to nearly $28.7 trillion by the end of 2028. Publicly held debt differs from gross federal debt which includes funds the government owes itself, or intragovernmental debt.

Interest on debt

Just like a personal loan, the government pays interest on the money it borrows. The CBO projects that the net interest paid on its debt will nearly triple over the next decade from an estimated $316 billion in 2018 to $915 billion in 2028. A presumed climb in interest rates over the next few years factors in the exponential growth rate.

Debt as a percentage of GDP

The GDP, or gross domestic product, measures the value the goods and services produced by a country in a given period of time and indicates economic output. Some economists use as a gauge the national debt as a percentage of the GDP, and it has grown steadily after the 2008 recession. The CBO predicts the debt will rise to nearly 100 percent of the nation's GDP by 2028, which is the highest amount of debt relative to the size of the economy in the United States since 1946. The CBO cautions that growing debt can result in negative consequences such as less flexibility to respond to unexpected challenges and the risk of investors being unwilling to finance the government's borrowing.

projects.newsday.com/databases/long-island/deficits/#user=56e9c3e1487ccdac2d8bafde&utm_source=newsletter&utm_medium=email&utm_campaign=Morning-Update |

|

|

|

Post by the Scribe on Mar 30, 2020 8:32:12 GMT

The Federal deficit: Mulvaney says the congressional budget office was right after allCBO comes in lower than the White House — still, both numbers are really, really big

Salon.com 21 hours ago

This is definitely a man-bites-dog federal budget story.

Since becoming Trump’s Office of Management and Budget director, Mick Mulvaney has viciously attacked the Congressional Budget Office as a highly partisan and substantively inept organization. He has repeatedly questioned its economic assumptions, its budget analyses and the politics of its analysts.

And that makes it more than a little newsworthy that OMB, the federal agency Mulvaney himself directs and in his mind is a paragon of bipartisanship and objectivity, released a report last Friday that not only shows that CBO’s numbers were substantively good, it also shows that the organization Mulvaney had attacked for being too partisan was more optimistic about where the federal deficit is headed the next few years than Trump’s own budget director.

CBO said in its Long-Term Budget Outlook report released last month that the 2018 deficit will be $793 billion; OMB said in its just-released Mid-Session Review of the president’s budget that it will be $890 billion. For 2019, CBO said the deficit will be $973 billion while OMB said it will be $1.085 trillion. For 2020, CBO said $1.003 trillion compared to OMB’s $1.076 trillion.

It’s important to note that OMB’s numbers are based on what we already know is a complete myth: that the spending cuts included in the Trump fiscal 2019 budget sent to Congress earlier this year will be enacted. For the second year in a row, the GOP Congress has shown no interest whatsoever in adopting the spending cuts the president proposed.

As a result, the disparity between CBO’s relatively optimistic deficit estimates and OMB’s comparatively pessimistic projections is most likely to get larger.

To be fair, CBO and OMB diverge in the opposite direction from 2022 through 2028. But, also to be fair, everyone’s budget forecast beyond three years is far more guesswork than substantive analysis given that its multiple congressional and presidential elections and countless natural and man-made disasters will occur, and long-term forecasts of how fast the economy will grow (or not) are often just wishful thinking or straight-line extrapolations.

In the meantime, however, OMB Director Mick Mulvaney owes the Congressional Budget Office a huge apology.

Stan Collender is one of the leading experts on the federal budget, federal spending and revenues, the deficit, the national debt and the congressional budget process. He blogs thebudgetguy and can be found on Twitter @thebudgetguy.

www.salon.com/2018/07/29/the-federal-deficit-mulvaney-says-the-congressional-budget-office-was-right-after-all_partner/

|

|

|

|

Post by the Scribe on Mar 30, 2020 8:33:20 GMT

Trader: "The US Is Closer To A Recession Than You Think"by Tyler Durden

Tue, 07/10/2018 - 08:37

Turn on the TV or spend any time on Twitter and you will be comfortably, numbly, reassured that everything is awesome - stocks are up (well FANGs are up), confidence is up (as is credit card debt), and the economy is "SOARING" (as long as you don't pay attention to the weakness in income growth). However, reality is that the so-called economic data that the mainstream relies upon is 'soft' survey-based perceptions skewed by 'hope' and 'expectations', and while that is rising once again, 'hard' real economic data continues to languish awkwardly unchanged from the start of President Trump's reign..

And while facing reality, especially as cognitive dissonance is running so hot, Bloomberg's Jacob Bourne has a timely warning that many will choose to ignore - Despite the momentum in the U.S. economy (solid jobs data, a robust earnings picture, fiscal stimulus), markets are trading like the next recession is drawing closer.

Bloomberg's markets recession model, which translates how various asset classes are trading into recession probabilities, now flags the next recession to take place in 12-24 months. More importantly, the start of the recession is more likely to be in the next 12 months rather than in two years.

Of course, this will not be discussed among the 'experts' because - simply put - there is always a risk that this becomes a self-fulfilling prophesy; after all, if enough people worry about a recession and shun riskier assets, they end up raising funding costs for corporations, resulting in the recession they were so worried about -- the perennial problem of the Keynesian beauty contest that characterizes the global economy.

With markets the ultimate judge of the contest, it all depends on how the world’s central banks react to the market signals... and if they do react, will that shatter the veil of ignorance so many traders rely on when they BTFTWD!!??

www.zerohedge.com/news/2018-07-10/us-closer-recession-you-think

|

|

|

|

Post by the Scribe on Mar 30, 2020 8:33:59 GMT

|

|

|

|

Post by the Scribe on Mar 30, 2020 8:34:40 GMT

With millions of baby boomers retiring and dying it is no wonder unemployment is low. Last I heard Trump had nothing to do with that fact. Where are the high wages Trump promised? Where is the great healthcare Trump promised? Where is the WALL paid for by Mexico Trump promised? So far all we got is the Trumpubliconservative Tax Reform Redistribution Act for the Wealthy that is adding trillions to our deficit and could decimate what little social safety net we have left unless Democrats get in to change things.AP FACT CHECK: Trump falsely claims economy, jobs best everAssociated Press CHRISTOPHER RUGABER,Associated Press 3 hours ago .

President Donald Trump speaks during a rally, Saturday, Aug. 4, 2018, in Lewis Center, Ohio. (AP Photo/John Minchillo)

WASHINGTON (AP) — President Donald Trump is grossly overstating the extent of U.S. economic and job gains.

In a tweet Monday, he declares that the economy has "never been better" and jobs are at the "best point in history."

In fact, the economy and jobs are nowhere close to historic bests based on several measures. Economists have also warned that U.S. growth is largely fueled by government borrowing, as the federal deficit rises because of his tax cuts, and is thus unlikely to be sustainable after a few quarters.

A look at the claims:

TRUMP: "Great financial numbers being announced on an almost daily basis. Economy has never been better, jobs at best point in history."

THE FACTS: He's exaggerating. The economy is healthy now, but it has been in better shape at many times in the past.

Growth reached 4 percent at an annual rate in the second quarter, which Trump highlighted late last month with remarks at the White House. But it's only the best in the past four years. So far, the economy is expanding at a modest rate compared with previous economic expansions. In the late 1990s, growth topped 4 percent for four straight years, from 1997 through 2000. And in the 1980s expansion, growth even reached 7.2 percent in 1984.

It's not clear what Trump specifically means when he declares that jobs are at the "best point in history," but based on several indicators, he's off the mark.

The unemployment rate of 3.9 percent is not at the best point ever — it is actually near the lowest in 18 years. The all-time low came in 1953, when unemployment fell to 2.5 percent during the Korean War. And while economists have been surprised to see employers add 215,000 jobs a month this year, a healthy increase, employers in fact added jobs at a faster pace in 2014 and 2015. A greater percentage of Americans held jobs in 2000 than now.

Trump didn't mention probably the most important measure of economic health for Americans — wages. While paychecks are slowly grinding higher, inflation is now canceling out the gains. Lifted by higher gasoline prices, consumer prices increased 2.9 percent in June from a year earlier, the most in six years.

Adjusting for inflation, hourly pay for non-managers — about 80 percent of the workforce — fell 0.2 percent over the same period. Yet in 1998, for example, inflation-adjusted hourly pay growth topped 2.5 percent.

___

Find AP Fact Checks at apne.ws/2kbx8bd

Follow @apfactcheck on Twitter: twitter.com/APFactCheck

EDITOR'S NOTE _ A look at the veracity of claims by political figures

www.yahoo.com/finance/news/ap-fact-check-trump-falsely-claims-economy-jobs-183130277.html

|

|

|

|

Post by the Scribe on Mar 30, 2020 8:35:36 GMT

GOP's budget-busting policies are downright shameful By Jonathan Bydlak, opinion contributor — 08/14/18 01:15 PM EDT 103comments

The views expressed by contributors are their own and not the view of The Hill

The Congressional Budget Office recently reported that the federal deficit jumped 20 percent in the first 10 months of the fiscal year, an eye-popping increase that was largely a result of two factors: the short-term impact of tax cuts and the big-spending agreements the Republican-led Congress has been passing with almost no dissent.

Perhaps unsurprisingly, voices on the left have begun caring about the deficit again — a chorus that is likely to continue for as long as they are in the minority. But despite the inevitable cries of hypocrisy against the few Republicans who voted for tax cuts and against big spending, there is a wide range of opinion among Republicans on how much to care about the short-term deficit impact of tax cuts.

Committed supply-siders, for example, will argue that long-term growth will more than make up for any shortfalls, but most Republicans don’t truly fit into that bucket. Many instead have made a calculation, perhaps a political one, that keeping more money in people’s pockets is more important than the potential harms of deficits.

Since we cannot mathematically tax our way to balance, why shouldn’t taxpayers get a break in the meantime?

But regardless of which camp one falls into, the idea that we have to pick between lower taxes and lower deficits is a false one. In fact, there is a straightforward means of keeping deficits in check while reducing taxes, but that option is largely being ignored despite years of promises from Republican leadership.

It’s hard to find a Republican who ran for office without calling to reform and reduce government spending — almost as hard as it is to find any now who seem to care as their party continues to ratchet up the spending.

There’s no shortage of bills that have passed, or are on the horizon, with massive price tags: last spring’s omnibus spending package, relief for farmers hurt by trade wars as well as a massive farm bill likely to become law soon.

The latest National Defense Authorization Act was signed on Monday, and there are few signs that upcoming Department of Defense appropriations will include many reforms.

The level and rate of high spending has seemed to shock even President Trump, who signed and promptly blasted the $1.3 trillion spending bill in March of this year, saying he nevertheless had no choice because military spending was on the line.

Herein lies the other, bigger problem. Congress simply doesn’t budget anymore, much less thoughtfully. Because the broken budget process has proven impossible to complete in time, lawmakers have become a rubber stamp for whatever big-spending deal leadership can cobble together, which they pass at the last minute with almost no one willing to say no.

And if reforming discretionary spending is becoming a distant dream, doing anything to fix the two-thirds of the budget that is on autopilot seems all but impossible.

This problem has existed under Republican and Democratic administrations, but the closer Washington inches toward insolvency, the less defensible it becomes.

Eventually — or much sooner than that — this irresponsibility will have severe consequences, as major programs simply run out of money, and many years of kicking the can create unavoidable pain.

In just 30 years, interest on the debt is projected to be a bigger liability than Social Security and national defense, and in a best-case scenario — with a steady economy and no unexpected military ventures — the country will see priorities squeezed with little in the way of a backup plan.

The fact that this situation is happening to begin with is a shame; the fact that Republicans who have spent years promising to fix the debt are at the helm as it inches closer to crisis is nothing short of shameless hypocrisy.

Jonathan Bydlak is the founder and president of the Coalition to Reduce Spending and the creator of SpendingTracker.org.

|

|

|

|

Post by the Scribe on Mar 30, 2020 8:36:43 GMT

I don't know about you but everything I usually buy on a regular basis has been steadily increasing in price. My utility costs are going through the roof as well. Local and state taxes are going up to make up for the the Republicon Tax Reform Act for the Wealthy. Revenues have to be made up somewhere and it falls onto the middle class. And that is just in anticipation of the cuts. Wait until it all kicks in next year.U.S. consumers have no tolerance for inflationMyles Udland 2 hours 45 minutes ago .

In July, core inflation in the U.S. notched its biggest annual increase since September 2008.

In August, consumers noticed.

In August, U.S. consumers changed their view of the U.S. economy as inflationary pressures have perked up in recent months. (AP Photo/Julio Cortez)

According to the University of Michigan’s first look at consumer sentiment in August released Friday, consumers’ assessment of current economic conditions declined due to, “much less favorable assessments of buying conditions, mainly due to less favorable perceptions of market prices.”

In other words, things got more expensive and consumers pulled back.

The University of Michigan’s headline consumer sentiment index slipped to 95.3 in the beginning of August, down from 97.9 at the end of July and the lowest reading in 11 months. The decline in consumers’ assessment of current economic conditions also declined to 107.8 from 11.4 in July, its lowest level in almost two years. Since Trump’s election, consumer confidence surveys have indicated consumers are feeling as good as they have since the early 2000s.

And when it comes to big-ticket items for households, the outlook in August was even worse.

“Buying conditions for large household durables sank to the lowest level in nearly four years,” said Richard Curtin, chief economist for the survey.

“When asked to explain their views, consumers voiced the least favorable views on pricing for household durables in nearly ten years, since October 2008. Vehicle buying conditions were viewed less favorably in August than anytime in the last four years, with vehicle prices being judged less favorably than anytime since the close of 1984. Home buying conditions were viewed less favorably in early August than anytime in the past ten years, with home prices judged less favorably than anytime since 2006.” (Emphasis added.)

In July, “core” inflation — which strips out the more volatile costs of food and gas — rose 2.4% over the prior year, the most since September 2008. Headline inflation which captures the costs of food and gas rose 2.9% over last year, in-line with the rise seen in June that was good for a six-year high.

Curtin added that these changes in consumers’ view of current conditions are “extraordinary” given that the outlook for inflation from consumers was unchanged from July; consumers still expect inflation in the year ahead to be 2.9%.

The broader upshot for markets from Friday’s report is that U.S. consumers may start to change their spending habits before economists and other experts see conditions as stressed.

“The data suggest that consumers have become much more sensitive to even relatively low inflation rates than in past decades,” Curtin added.

And with President Trump’s tariffs pushing up the cost of goods like washing machines in recent months and these moves increasing the cost of inputs across industries — and thus leading to higher consumer prices — it seems unlikely inflationary pressures will abate.

This is a trend that appears to already be causing consumers to change their spending habits and their view on the U.S. economy.

www.yahoo.com/finance/news/u-s-consumers-no-tolerance-inflation-161959788.html

|

|

|

|

Post by the Scribe on Mar 30, 2020 8:37:37 GMT

This seems to be the m.o. of all republiconservatives. Borrow and spend. At least the tax and spend Democrats make sure they have money from taxes to pay for things. And then the cons either crash the economy or leave the problems to a liberal president to get things back in order. They then scream about deficits and want the social safety net destroyed.Trump trillion-dollar-plus deficits are putting America on a path to fiscal ruinStan Collender, Opinion contributorPublished 6:00 a.m. ET Aug. 20, 2018 | Updated 2:08 p.m. ET Aug. 20, 2018

Though no one in Washington will admit it, our nation's finances are in deep trouble. Spending is up, revenue is down, and this will only get worse.

(Photo: Michael Reynolds/epa-EFE)

It became very clear this month that neither the Trump White House nor its allies on Capitol Hill want you to know that the federal budget is already in very bad shape ... and getting worse.

It happened when the Treasury, the official keeper of Washington’s financial results, issued its monthly statement for the first 10 months of fiscal 2018 about federal revenue, spending and, therefore, the budget deficit.

Treasury showed what no president ever wants to admit: The deficit is spiking. The federal government’s red ink this year is already 21 percent above what it was in 2017, and there are few prospects that the bottom line will improve anytime soon.

Except with infrequent and unsubstantiated platitudes about how the situation is going to get better, the Trump White House and Republicans in Congress have been doing everything possible not to talk about the budget this year. To avoid tough questions and politically embarrassing votes, the House and Senate have even refused to consider a budget even though they are required by law to adopt one.

But this year isn’t the real issue.

Trump's deficits are permanent

Unlike the trillion dollar budget deficits that occurred during the Obama administration that were temporary and largely the result of the Great Recession, the Trump deficits that will soon reach and exceed $1 trillion are permanent and will only get worse in the years ahead.

The Trump deficits are the result of changes in federal spending and revenue that will continue to be in place until some president and Congress decide to reverse them, that is, to increase taxes and make cuts to popular programs.

Not only has there been little appetite to do that, many in Congress and the Trump administration seem to be hellbent on ignoring the deficit and national debt and increasing spending and reducing revenue even further.

President Trump directed the Department of Defense to begin plans to form a U.S. Space Force. The idea of forming a sixth military branch shocked some, but it’s not a new idea. Here’s how we got here. Just The FAQs

For example, the White House last week proposed a new Space Force that would likely add billions, if not hundreds of billions, to the Pentagon’s budget. Trump has asked for $25 billion for the wall he wants to build between the U.S. and Mexico. His much talked about but still unseen infrastructure plan would cost countless billions more.

www.usatoday.com/story/opinion/2018/08/20/donald-trump-trillion-dollar-plus-deficits-fiscal-ruin-column/986236002/

|

|

|

|

Post by the Scribe on Mar 30, 2020 8:38:25 GMT

So what does he do? Trumpubliconservaties give the 1% a 2 trillion dollar tax break.Donald Trump's $20 Trillion ProblemVisual Capitalist

Published on Jan 12, 2017

The 45th President of the United States will have to deal with many pressing issues including immigration, foreign policy, and the economy. But for many, one issue looms above all others: how will Donald Trump deal with the $20 trillion U.S. national debt? |

|

|

|

Post by the Scribe on Mar 30, 2020 8:39:29 GMT

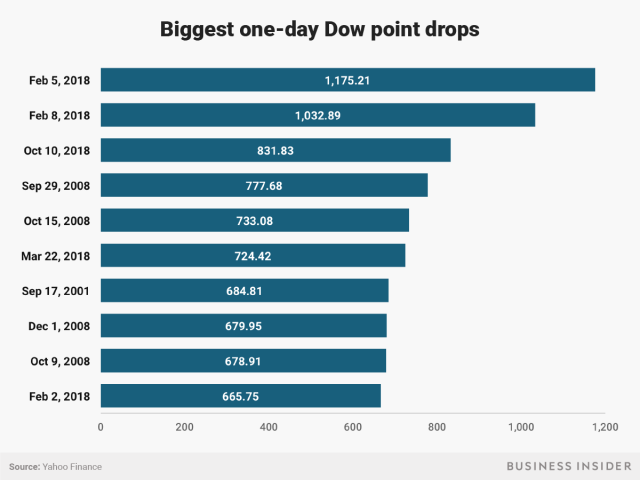

HURRICANE FED: Just like a hurricane does to cool down the planet, so does the Fed raise rates to cool down the economy. Trump blames the FED. Notice that half of the biggest one day point drops fell under King Trump's rule?Here are the biggest one-day point drops in the Dow's historyBusiness Insider Andy Kiersz,Business Insider 9 hours ago .

Stocks tumbled on Wednesday.

The Dow Jones industrial average fell 831.83 points, the third-largest one-day point drop in history.

Previous large one-day drops include several days during the financial crisis, and the first trading day after the September 11, 2001 terror attacks.

The stock market took a tumble Wednesday amid fears surrounding global growth, rising interest rates, and trade disputes.

The Dow closed down 831.83 points, the third-largest one-day point drop in its history.

The biggest one-day point drop came earlier this year. On February 5, the Dow fell 1,175.21 points. The previous holder of that dubious honor was September 29, 2008, when the Dow dropped 777.68 points after the first version of the TARP bailout program failed in Congress.

It's worth noting that these are point drops and not percentage drops. As the Dow has gotten steadily higher over the last several decades, larger point drops translate into smaller percentage drops. Wednesday saw a 3.2% decline, which while far more tumultuous than we've seen in some time, pales in comparison to the 22.6% decline the Dow suffered on Black Monday in 1987, or the 12.8% drop experienced during the 1929 stock crash.

Here are the 10 biggest one-day point drops in the Dow's history.

|

|

|

|

Post by the Scribe on Mar 30, 2020 8:41:56 GMT

And another factoid: The other big point drops happened during Son-Of-A-Bush's presidency. Trump Hits A New High-Water Mark: The Biggest Federal Deficit In 6 YearsHuffPost

Mary Papenfuss,HuffPost•October 15, 2018

President Donald Trump likes to boast that he’s breaking records with the latest low unemployment figures. Here’s another record for his administration: The 2018 federal deficit hit the highest level of the last six years.

The deficit jumped 17 percent (or by $113 billion) to $779 billion at the end of Trump’s first fiscal year, according to final figures released Monday by the Treasury Department. That’s mostly due to the massive corporate tax cut that slashed rates from 35 percent to 21 percent, choking revenue for spending, which climbed 3 percent. Much of that was a hike in defense spending and money to pay interest on the climbing federal debt, CNN reported.

The U.S. government’s $523 billion in interest payments to service its debt in 2018 — the highest ever — was more than the entire economic output of Belgium this year, Bloomberg reported.

Corporate tax collections in the U.S. fell 22 percent, or $76 billion, in the fiscal year, which ended Sept. 30.

The total federal debt — which combines annual deficits — was 78 percent of the nation’s entire gross domestic product in June. It hasn’t been that large a percentage since World War II.

Trump promised the tax cuts would pay for themselves by boosting business, which would produce more taxes. But that hasn’t yet happened. The Trump administration estimates that the deficit will increase to $1.09 trillion in the next fiscal year.

The federal government usually increases spending — and deficits — to boost a faltering economy — such as during the 2008 recession triggered by the subprime mortgage and banking crisis. But the economy was already in a strong recovery when Trump moved into the White House, and he still boosted the deficit.

“By cutting taxes in 2017 when the economy was already quite strong, Congress and the administration not only missed a golden opportunity to begin to address the fiscal problem, they actually made the problem worse,” William Gale, a senior fellow at the Brookings Institution, told CBS News.

The GOP had traditionally been the party that battled for a balanced federal budget.

Bernie Sanders

✔

@sensanders

4 Republican policies led to a $779 billion deficit in 2018:

- Bush Tax Cuts: $488 B

- Trump Tax Cuts: $164 B

- Wars in Iraq and Afghanistan: $127 B

- Defense increases since 9/11: $156 B

Without tax cuts for the wealthy and endless wars we would've had a $156 billion SURPLUS.

2:03 PM - Oct 15, 2018

15.4K

6,800 people are talking about this

Twitter Ads info and privacy

This article originally appeared on HuffPost.HERE IT COMES October 15, 2018, 4:52 PMFederal budget deficit hits 6-year-high in Donald Trump's first fiscal year as presidentTreasury Secretary Steve Mnuchin suggested in a statement that the underlying source of the widening deficit was growth in government spending, rather than the tax cuts.

"Going forward the President's economic policies that have stimulated strong economic growth, combined with proposals to cut wasteful spending, will lead America toward a sustainable financial path," Mnuchin said.

But William Gale, a senior fellow at the Brookings Institution, noted that the tax cuts are unlikely to generate a long-term bump in economic growth. More importantly, most estimates suggest that the deficit will worsen as spending on Social Security, Medicare and other programs increase with the aging baby boomer population.

|

|

|

|

Post by the Scribe on Mar 30, 2020 8:42:56 GMT

We now know the real winners of the Trump tax cutsRick Newman

Senior Columnist

Yahoo FinanceOctober 15, 2018

Less than a month before the midterm elections, government data shows that business tax payments plunged in fiscal 2018, which ended in September—while individual taxpayers paid more.

President Trump and Congressional Republicans who passed the tax cuts late last year, without any Democratic support, figured voters would thank them for the extra spending money, come Election Day. But that may not happen. More people oppose the tax cuts than favor them, and 64% say they’ve seen no change in their take-home pay on account of the tax cuts.

It’s party time in the corporate sector, however, with tax cuts generating an earnings boom and keeping a shaky stock-market rally intact. Corporate profits jumped 15.4% year-over year in the first half of 2018, compared with a rise of just 6.1% in the first half of 2017, before the tax cuts went into effect. That’s the biggest semi-annual jump in profits since 2012.

Louise Linton and her husband, Treasury Secretary Steve Mnuchin, in Nov. 15 with a sheet of new $1 bills. (AP Foto/Jacquelyn Martin)

Income gains for ordinary workers have been more muted, averaging just 2.8% so far this year. And while corporate profits have soared to new record highs, household earnings have only recently recovered years of losses, leaving many families feeling like they’re barely getting ahead.

The Trump tax cuts are unpopular because many people feel they benefit businesses and high earners more than middle-class workers. This year’s tax-receipt numbers back that up. Individual income-tax receipts rose from $1.587 trillion in fiscal 2017 to $1.684 trillion in 2018. That’s a 6.1% increase. Much of that is due to a growing economy and population growth.

Cut in corporate tax rate

Business-tax receipts, by contrast, plunged from $297 billion in 2017 to $206 billion in 2018, a 31% decline driven by the cut in the corporate tax rate from 35% to 21%. The portion of federal revenue that comes from business taxes has been dropping for years, and it fell from 7.5% in 2017 to 5% in 2018. Individual income-tax payments account for 41% of federal revenue.

The annual deficit rose from $666 billion in 2017 to $779 billion in 2018. And that’s with the tax cuts in effect for just eight of 12 months. The deficit could top $1 trillion in fiscal 2019, and stay above that for the foreseeable future.

Trump and his economic advisers insist that ballooning budget deficits aren’t a problem, because the tax cuts are stimulating economic growth in a way that will eventually boost federal revenues through higher incomes. But many economists say this supply-side theory has never occurred, in reality. And it’s plain in the numbers that the Trump tax cuts, so far, are adding to government debt, not reducing it.

Another worrying sign in the 2018 budget numbers is the amount spent on interest payments, which jumped 24%, from $263 billion in 2017 to $325 billion in 2018. The U.S. government has been able to borrow very cheaply during the last several years, because of super-low rates on U.S. Treasury securities. But rates are going up, which will force taxpayers to spend more on interest and, eventually, less on everything else.

“It’s an unsustainable fiscal course,” Maya MacGuineas, president of the Committee for a Responsible Federal Budget, said in a statement. “Those elected to Congress this year will face stark and difficult choices to put the debt on a downward path.” Voters may have that in mind as they decide who those people will be.

Confidential tip line: rickjnewman@yahoo.com. Click here to get Rick’s stories by email.

Read more:

•Trump’s new plan to help struggling workers

•The rich–poor gap is getting worse under Trump

•Why this Texas business owner loves the Trump tariffs

•Trump’s big strategy on trade: Rebranding

•Some business owners love the Trump tariffs

•Some Republican approve of Russia’s help in elections

•Socialists are coming for the Democratic party

finance.yahoo.com/news/business-tax-payments-plunged-2018-203650862.html

|

|