|

|

Post by the Scribe on Apr 8, 2020 23:38:33 GMT

Deductions were eliminated for the middle and lower incomes and increased for the upper incomes. As far as increased income during the year, inflation wiped out any middle and lower income gains. Supply side is a tax break for the rich, always. Claims of it benefiting the entire economy have been repeatedly disproven by it's application. Fox & Friends accidentally admits ON AIR the truth about Trump's tax bill  |

|

|

|

Post by the Scribe on Apr 8, 2020 23:39:13 GMT

|

|

|

|

Post by the Scribe on Apr 8, 2020 23:39:49 GMT

ECONOMICS 101 LABOR CREATES WEALTH, NOT THE OTHER WAY AROUND....SOMEONE SEND THE MEMO TO REPUBLICONSERVATIVES(and LABOR should be sharing in the wealth otherwise it is slavery)the Nick Hanauer banned TED talk is available

Banned TED Talk: Nick Hanauer "Rich people don't create jobs"

Zubenelgenubiii

5.71K subscribers

Via Business Insider: "As the war over income inequality wages on, super-rich Seattle entrepreneur Nick Hanauer has been raising the hackles of his fellow 1-percenters, espousing the contrarian argument that rich people don't actually create jobs. The position is controversial — so much so that TED is refusing to post a talk that Hanauer gave on the subject. National Journal reports today that TED officials decided not to put Hanauer's March 1 speech up online after deeming his remarks "too politically controversial" for the site...".

Beware, fellow plutocrats, the pitchforks are coming | Nick Hanauer

TED

14.8M subscribers

Nick Hanauer is a rich guy, an unrepentant capitalist — and he has something to say to his fellow plutocrats: Wake up! Growing inequality is about to push our societies into conditions resembling pre-revolutionary France. Hear his argument about why a dramatic increase in minimum wage could grow the middle class, deliver economic prosperity ... and prevent a revolution.

Banned TED Talk |

|

|

|

Post by the Scribe on Apr 8, 2020 23:40:29 GMT

"Trump's tax overhaul can disproportionately impact blue states, judge rules": Well yeah. That was done intentionally by the "Elections have consequences for you" Republicans. Republicans want you to know if you aren't with them you're gonna pay. The thing is, Blue State liberals will move to less expensive Red States and will bring their liberal values with them and VOTE that way. Conservatives are short thinking suckers and crybullies.Judge rules that Trump's tax overhaul can disproportionately impact blue states Alexis Keenan 2 hours 2 minutes ago

www.yahoo.com/finance/news/trump-tax-law-state-salt-205820313.html

A Manhattan federal district judge on Monday issued bad news for taxpayers hoping to sidestep the Trump administration’s cap on state and local tax deductions.

For now, the decision means that all federal taxpayers who itemize deductions remain subject to the rule first effective for the 2018 tax year, which limits such “SALT” deductions to $10,000.

In December 2017, President Donald Trump signed into law the Tax Cuts and Jobs Act Trump, which reformed the tax code to limit total state and local taxes to a $10,000 maximum for single filers and married couples filing jointly, and $5,000 for married couples filing separately.

Four U.S. states that collectively challenged the administration’s SALT cap — New York, New Jersey, Connecticut, and Maryland — had their case dismissed, the judge reasoning the states failed to show the cap was unconstitutional, or beyond Congress’ authority. The states said they were home to “the highest percentages of taxpayers whose federal tax burden increased” under the new rule. All four are Democratic-leaning states.

USA tax return 1040s

Image: Getty

‘An invasive and unprecedented attempt’

New York Attorney General Letitia James called the administration’s limitation “an invasive and unprecedented attempt by the federal government to curtail” state constitutional rights. James said her office was reviewing the decision as it considered its available options. That could include an appeal. “We remain committed to defending our taxpayers and our state,” she said.

NEW YORK, NY - JUNE 11: New York Attorney General Letitia James speaks during a press conference, June 11, 2019 in New York City. James announced that New York, California, and seven other states have filed a lawsuit seeking to block the proposed merger between Sprint and T-Mobile. James said that the merger would deprive customers of the benefits of competition and potentially drive up prices for cellphone service. (Photo by Drew Angerer/Getty Images)

The law unfairly targets blue states, the states’ attorneys general argued, in advocating to maintain the old rule on SALT deductions that would largely benefit homeowners.

Judge Paul Oetken, who was appointed by Obama, concluded that the states failed to “plausibly” claim that the cap constrains states’ sovereign tax power decision-making any differently than under other major federal initiatives.

“In the end, Congress enacted the SALT cap pursuant to its broad tax powers under Article I, section 8 and the Sixteenth Amendment,” Judge Oetken wrote in his decision. “The cap, like any federal tax provision, will affect some taxpayers more than others and, by extension, will affect some states more than others.”

New York’s lawyers argued that its taxpayers would collectively pay $121 billion more in federal taxes between 2018 and 2025 than without the $10,000 cap. The state’s filers who itemized deductions under the old rule claimed $21,943, on average.

New Jersey, Connecticut, and Maryland argued that in 2018, alone, taxpayers from their states paid $7.5 billion more to the federal government than they would have paid without the cap.

Alexis Keenan is a reporter for Yahoo Finance. She previously worked for CNN and is a former litigation attorney. Follow on Twitter @alexiskweed. |

|

|

|

Post by the Scribe on Apr 8, 2020 23:41:07 GMT

Trump’s Trillion-Dollar Hit to HomeownersBy reducing deductions for real estate taxes, Trump’s 2017 tax plan has harmed millions — and helped give corporations a $680 billion gift.

by Allan Sloan Oct. 10, 5 a.m. EDT

www.propublica.org/article/trumps-trillion-dollar-hit-to-homeowners#168716

Daniel Savage, special to ProPublica

ProPublica is a nonprofit newsroom that investigates abuses of power. Sign up for ProPublica’s Big Story newsletter to receive stories like this one in your inbox as soon as they are published.

This story was co-published with Fortune.

In recent weeks, President Donald Trump has been talking about plans for, as he put it, a “very substantial tax cut for middle income folks who work so hard.” But before Congress embarks on a new tax measure, people should consider one of the largely unexamined effects of the last tax bill, which Trump promised would help the middle class: Would you believe it has inflicted a trillion dollars of damage on homeowners — many of them middle class — throughout the country?

That massive number is the reduction in home values caused by the 2017 tax law that capped federal deductions for state and local real estate and income taxes at $10,000 a year and also eliminated some mortgage interest deductions. The impact varies widely across different areas. Counties with high home prices and high real estate taxes and where homeowners have big mortgages are suffering the biggest hit, as you’d expect, given the larger value of the lost tax deductions. But as we’ll see, homeowners all over the country are feeling the effects.

I’m basing my analysis on numbers from two well-respected people: Mark Zandi, the chief economist of Moody’s Analytics; and Hugh Lamle, the retired president of M.D. Sass, a Wall Street investment management company.

Zandi’s numbers are broad — macro-math, as it were. Lamle (pronounced LAM-lee) is a master of micro-math. It was Lamle who first got me thinking about home value losses by sending me an economic model that he created to show the damage inflicted on high-end, high-bracket taxpayers in high-tax areas who paid seven digits or more for their homes.

Lamle starts with the premise that homebuyers have typically figured out how much house they can afford by calculating how much they can spend on a down payment and monthly mortgage payment, adjusting the latter by the amount they’d save via the tax deduction for mortgage interest and real estate taxes. His model figures out how much prices would have to drop for the same monthly payment to cover a given house now that this notional buyer can’t take advantage of the real estate tax deduction and might not be able to take full advantage of the mortgage interest deduction.

After I showed Lamle’s model to my ProPublica research partner, Doris Burke, she steered me to Zandi’s research, which I realized could be used to calculate national value-loss numbers.

Ready? Here we go. The broad picture first, then the specific. This gets a little complicated, so please bear with me.

Zandi says that because of the 2017 tax law, U.S. house prices overall are about 4% lower than they’d otherwise be. The next question is how many dollars of lost home value that 4% translates into. That isn’t so hard to figure out if you get your hands on the right numbers.

Let me show you.

The Federal Reserve Board says that as of March 31, U.S. home values totaled about $26.1 trillion. Apply Zandi’s 4% number to that, and you end up with a $1.04 trillion setback for the nation’s home owners. That’s right — a trillion, with a T.

Please note that Zandi isn’t saying that house prices have fallen by an average of 4%. That hasn’t happened. What he’s saying is that on average, house prices are about 4% lower than they’d otherwise be.

Given that the Fed statistics show that homeowners’ equity was $15.76 trillion as of March 31, Zandi’s numbers imply that homeowners’ equity is down about 6.6% from where it would otherwise be. (That’s the $1.04 trillion value loss divided by the $15.76 trillion of equity.)

This is a very big deal to families whose biggest financial asset is the equity they have in their homes. And there are untold millions of families in that situation.

While Zandi and I were having the first of several phone conversations, he sent me a county-by-county list of the estimated home-price damage done to about 3,000 counties throughout the country. I was fascinated — and appalled — to see that the biggest estimated value loss in percentage terms, 11.3%, was in Essex County, New Jersey, the New York City suburb where I live.

In case you’re interested — or just snoopy — the four other counties that make up the five biggest-losers list are: Westchester County, New York, suburban New York City, 11.1%; Union County, New Jersey, which is adjacent to Essex County, 11.0%; New York County, the New York City borough of Manhattan, 10.4%; and Lake County, Illinois, suburban Chicago, 9.9%.

Here’s how it works. Zandi took what financial techies call the “present value” of the property tax and mortgage interest deductions that homeowners will lose over seven years (the average duration of a mortgage) because of changes in the tax law and subtracted it from the value of the typical house. That results in a 3% decline in national home values below what they would otherwise be.

The remaining one percentage point of value shrinkage, Zandi says, comes from the higher interest rates that he says will result from the higher federal budget deficits caused by the tax bill. He estimates that rates on 10-year Treasury notes, a key benchmark for mortgage rates, will be 0.2% higher than they would otherwise be, which in turn will make mortgage rates 0.2% higher.

Even though interest rates on 10-year Treasury notes are at or near record lows as I write this, they would be even lower if the Treasury were borrowing less than it’s currently borrowing to cover the higher federal budget deficits caused by Trump’s tax bill.

If Zandi’s interest-rate take is correct — it’s true by definition, if you believe in the law of supply and demand — even homeowners who aren’t affected by the inability to deduct all their real estate taxes and mortgage interest costs are affected by the tax bill.

How so? Because higher interest rates for buyers translate into lower prices for sellers and therefore produce lower values for owners.

You can argue, as some people do, that real estate taxes should never have been deductible because allowing that deduction is bad economic policy that inflated home prices and favored higher-income people over lower-income people.

But even if you believe that, there’s no question that eliminating the deduction for millions of homeowners inflicted serious financial damage on homeowners who had no warning that a major tax deduction that they were used to getting would be wiped out.

As a result, homebuyers who had taken the value of the real estate tax deduction into account when buying their homes had their home values and finances whacked without warning. Interest deductions on mortgage borrowings exceeding $750,000 were cut back, compared with interest deductions on up to $1 million under the old law — but that doesn’t affect anywhere near as many people as the cap on real estate tax deductions does.

(A brief aside: Among the modest winners here are first-time buyers who purchased their homes after the tax law took effect and benefited by paying less than they would have paid under the old tax rules.)

Manhattan was one of the five biggest losers in Trump’s 2017 tax plan. The value of residential real estate in New York County is 10.4% lower than it would otherwise be. (Drew Angerer/Getty Images)

Now, to the micro-math.

Lamle’s model isn’t applicable to most people because it works only for taxpayers with a household income of at least $200,000 a year who paid at least $1 million for their homes. But the principle underlying Lamle’s model applies to everyone who owns a home or is interested in owning one. To wit: You calculate the tax-law-caused loss of value by figuring out how much a house’s price needs to fall for buyers’ or owners’ after-tax costs to be the same now as they were before the tax law changed.

“People buying large-ticket items typically focus on after-tax costs of ownership,” Lamle told me. “The amount that many buyers can afford is affected by limits on their financial resources. Therefore, as their tax costs increase substantially because of the loss of tax deductions, they have less money available to pay for homes and to take on mortgage debt.”

At the suggestion of one of my editors, I asked Lamle to use a modified version of his economic model to estimate the tax law’s impact on the value of a theoretical house in the New York City suburb of West Orange, New Jersey, purchased for $800,000 in 2017 by a theoretical family with a $250,000 annual income. Those home value and income numbers are very high by national standards — but middle class by the standards of large parts of suburban Essex County.

Real estate tax on that theoretical house would run about $28,900 a year, according to statistics from the New Jersey state treasurer’s office. That tax used to be fully deductible for federal tax purposes. Now, it’s not deductible at all if you assume that the house’s owners are taking the standard deduction on their federal returns. Or that even if they’re itemizing deductions, they’re paying at least $10,000 of state income taxes, which means they don’t get any benefit from deducting property taxes.

According to Lamle’s calculations, this inability to deduct real estate tax has reduced the home’s value by $138,720, assuming a 5% mortgage rate. At a 4% rate, the value loss is $173,400. (For the math and assumptions underlying these numbers, see his methodology below.) So if the family put up $200,000 — 25% of the purchase price — to buy the house, more than half of that investment has been wiped out.

Obviously, it’s impossible to prove that Zandi and Lamle are right about the impact they say the tax law is having (and will continue to have) on home prices, because there’s no way to gauge the accuracy of their numbers. But the logic is compelling.

The loss in home values is crucial because it turns out that lots more people have bigger financial stakes in their houses than in their stock portfolios, which have thrived as the Trump tax law turbocharged corporate earnings and stock prices.

In fact, 73.5% of households that own homes, stocks or both had bigger stakes in the home market than in the stock market, according to David Rosnick, an economist at the Center for Economic and Policy Research, who parsed Federal Reserve data at my request.

Flawed Assessments Caused $2 Billion Shift in Property Taxes, Study Finds

Now, let’s put things in perspective, set aside home value losses for a minute and talk about the cash that people are getting from Trump’s 2017 tax law. It isn’t all that much for most families. Households’ average federal income tax has fallen by $1,260 a year, according to the Tax Policy Center. That average is skewed by big savings realized by people with big incomes; the median family’s tax cut is only about half as much as the average cut, by the Tax Policy Center’s math.

This means that means that — for taxpayers of higher income and more modest income — the income tax savings are likely small beer compared with the hidden loss inflicted on many of them by lower house values.

Back to the main event. And some final — but important — numbers.

According to the Tax Policy Center, the Treasury will get $620 billion of additional revenue over a 10-year period because people can’t deduct their full state and local taxes.

That, in turn, covers most of the 10-year, $680 billion cost of the income tax break that corporations are getting. So you can make a case that my friends and neighbors and co-workers in New York and New Jersey — and many of you all over the country — are paying more federal income tax in order to help corporations pay less federal income tax.

That, my friends, is the bottom line.

Dinged by the 2017 Tax Bill

Applying the formula devised by economist Mark Zandi, which estimates the effect of the tax bill on house values, the 30 counties below saw the biggest percentage declines.

County State % Change

Essex NJ -11.3%

Westchester NY -11.1%

Union NJ -11.0%

New York NY -10.4%

Lake IL -9.9%

Bergen NJ -9.9%

Passaic NJ -9.8%

Somerset NJ -9.8%

Mercer NJ -9.6%

Hunterdon NJ -9.6%

Gloucester NJ -9.5%

Nassau NY -9.4%

Fairfield CT -9.4%

Camden NJ -9.2%

Morris NJ -9.0%

Hudson NJ -9.0%

Rockland NY -8.7%

Putnam NY -8.7%

Kendall IL -8.7%

McHenry IL -8.4%

Burlington NJ -8.3%

Sussex NJ -8.2%

Middlesex NJ -8.0%

Hartford CT -7.6%

Will IL -7.5%

DuPage IL -7.4%

Monmouth NJ -7.3%

Orange NY -7.3%

Montgomery TX -7.2%

Warren NJ -7.1%

Source: Mark Zandi/Moody’s Analytics

Lamle’s Methodology

Here are the assumptions underlying the calculations of the value loss of a theoretical West Orange, New Jersey, house purchased for $800,000 in 2017.

The mortgage our theoretical buyers took out is less than $750,000, so all the interest on it would remain tax deductible for a family that files an itemized federal tax return.

The family’s federal income tax rate on each additional dollar of income is 24%.

The real estate tax on the house is about $28,900.

Therefore, those now-lost federal tax deductions would have been worth about $6,936 a year: 24% of $28,900. Under the law as it existed before the 2017 tax bill, buyers would typically have included those federal tax savings in calculating how much they could afford to pay for the house. Now, they don’t include those savings because they no longer exist. That’s because the real estate taxes aren’t deductible if the family takes the new, larger standard deduction. Or if the family continues to take itemized deductions — and if, as we assume, it pays at least $10,000 of state income taxes — the real estate taxes don’t provide any federal tax benefit.

Running those $6,936 of lost deductions through Hugh Lamle’s economic model produces indicated value losses of $138,720 for a 5% mortgage and $173,400 for a 4% mortgage.

This is conservative math. When the house’s current owners purchased it in 2017, their federal tax bracket would have been 28% rather than the current 24%. So the value of their now-lost federal tax deduction was $8,092 a year. That would imply value losses about 17% greater than those in the article.

Doris Burke contributed reporting to this story. |

|

|

|

Post by the Scribe on Apr 8, 2020 23:41:43 GMT

The Committee for a Responsible Federal Budget is coming up with their own ideas for what is being proposed in this campaign season. If it were up to me I would lower the age for Medicare to 50 years old. Allow anyone under that age to "buy into" it. Put stringent regulations on the Medicare Advantage Programs (Private Insurance Companies) and if this appears to be working lower the age for Medicare again and then again until everyone is covered. www.crfb.org/

The Democratic plan for a 42% national sales tax Rick Newman 2 hours 40 minutes ago

www.yahoo.com/finance/news/the-democratic-plan-for-a-42-national-sales-tax-202549219.html

If you’re a Democrat who supports “Medicare for All,” pick your poison. You can ruin your political career and immolate your party by imposing a ruinous new sales tax, a gargantuan income tax hike or a surtax on corporate income that would wreck thousands of businesses.

This is the cost of bold plans.

Supporters of Medicare for All, the huge, single-payer government health plan backed by Bernie Sanders, Elizabeth Warren and several other Democratic presidential candidates, say it’s time to think big and move to a health plan that covers everyone. Getting there is a bit tricky, however. A variety of analyses estimate that Medicare for All would require at least $3 trillion in new spending. That’s about as much tax revenue as the government brings in now. So if paid for through new taxes, federal taxation would have to roughly double.

The Committee for a Responsible Federal Budget (CRFB) has done voters a favor by spelling out what kinds of new taxes it would take to come up with that much money. Warren justifies many of her programs by saying all it would take is “two cents” from the wealthy. That’s a reference to her 2% wealth tax on ultra-millionaires. But Medicare for All would be so expensive that if you taxed top earners at 100%—that’s right, if you took all the income of couples earning more than $408,000 per year—you’d still fall far short. And everybody getting taxed at 100% would obviously stop working.

Okay, that won’t do it. So what will? CRFB outlined a variety of options. A 42% national sales tax (known as a valued-added tax) would generate about $3 trillion in revenue. But it would destroy the consumer spending that’s the backbone of the U.S. economy. A tax of that magnitude would be like 42% inflation, wrecking consumer budgets and the many companies that depend on them, from Walmart and Amazon to your local car dealer.

FILE - In this July 30, 2019 file photo, Sen. Bernie Sanders, I-Vt., and Sen. Elizabeth Warren, D-Mass., embrace after the first of two Democratic presidential primary debates hosted by CNN in the Fox Theatre in Detroit. (AP Photo/Paul Sancya)

Other options include a 32% payroll tax split between employers and workers or a 25% income surtax on everybody. Or, the government could cut 80% of spending on everything but health care, which would include highways, airports and the Pentagon. Or here’s a good one: Just borrow the money and quadruple Washington’s annual deficits.

The best idea might be charging every enrollee in the new program $7,500 per year, so they’d be paying directly for the coverage they’re getting. Some people pay more than that now for health care, by purchasing insurance outright or sacrificing pay raises in exchange for employer coverage. It would still be a nifty trick to propose that to voters.

The upside to these impossibly draconian scenarios is that nobody would pay anything for health care, except in the $7,500 example. And it’s possible that Medicare for All would cover health care for more people at a lower total cost than we spend now, meaning the average cost per person would go down. The problem is transitioning from what we have now to whatever Medicare for all would be. And it’s a giant problem, like crossing the Mississippi River without a bridge or a boat. The other side might look great but you’ll die before you get there.

Warren, Sanders and others tout the virtues of this magical health care program without explaining what it would cost. Sanders has at least suggested some possible ways to pay for it, including premiums paid by enrollees, a wealth tax on millionaires and income tax rates as high as 52%. Warren has been cagier, saying only that under her plan “costs” would go down for middle-class families. Under pressure to explain, Warren has pledged to come up with a financing plan soon. Now, maybe she doesn’t have to.

Rick Newman is the author of four books, including “Rebounders: How Winners Pivot from Setback to Success.” Follow him on Twitter: @rickjnewman. Confidential tip line: rickjnewman@yahoo.com. Encrypted communication available. Click here to get Rick’s stories by email.

Read more:

The staggering cost of Elizabeth Warren’s plans: $4.2 trillion per year finance.yahoo.com/news/the-staggering-cost-of-elizabeth-warrens-plans-42-trillion-per-year-161552386.html

Joe Biden’s health plan looks like the winner finance.yahoo.com/news/joe-biden-health-plan-medicare-for-all-040109177.html

There aren’t enough doctors for Medicare for all finance.yahoo.com/news/there-arent-enough-doctors-for-medicare-for-all-195947805.html

Why Democrats bomb with rural voters finance.yahoo.com/news/why-democrats-bomb-with-rural-voters-192130699.html

4 problems with Andrew Yang’s free money drop finance.yahoo.com/news/4-problems-with-andrew-yangs-free-money-drop-133802798.html

Read the latest financial and business news from Yahoo Finance

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit. |

|

|

|

Post by the Scribe on Apr 8, 2020 23:42:17 GMT

Republistupids have made it so a guy working 40 hours/week pays higher tax rates than a guy who inherited his wealth and lays around collecting dividends. So I pay more in taxes than the president of the USA and most large corporations. The Republiconservative Trump tax reform act was just a big give away to corporations and the wealthy. 84% of the stock market is owned by 10% of the population, and yet we continue to treat it like a scoreboard on the American economy. Trump is talking about going after SS and Medicare, taking away home interest credit. Someone has to make up the $1.5B that wasn't paid. Hope you're all so proud that your taxes are going to keep the wealthy wealthier. Trump followers actually believe he's a genius, but what they don't realize, Trump's corporate & wealthy tax cut allows the economy to sustain during his tenure hence making him look good. But Trump has done nothing but serve himself... Relatively speaking (and with some exceptions) the real genius behind this great economy will always be Obama. How Obama fixed Bush/Cheney's mess will never go unnoticed despite Trump's many attempts to tarnish his hard work. In essence, Trump did nothing. All he did was serve himself and the rest of the elite a sweet tax break while the working class got nothing but bottom tier jobs.

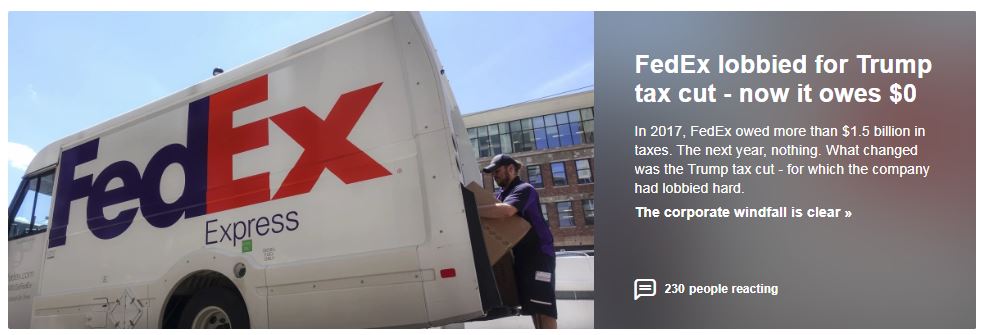

That is Trump's game, making Trump followers believe he's the great Caucasian hope when all he really is Don the Con.... How FedEx Cut Its Tax Bill to $0The New York Times Jim Tankersley, Peter Eavis and Ben Casselman,The New York Times 1 hour 33 minutes ago How FedEx Cut Its Tax Bill to $0The New York Times Jim Tankersley, Peter Eavis and Ben Casselman,The New York Times 1 hour 33 minutes ago

www.yahoo.com/news/fedex-cut-tax-bill-0-165617720.html

WASHINGTON — In the 2017 fiscal year, FedEx owed more than $1.5 billion in taxes. The next year, it owed nothing. What changed was the Trump administration’s tax cut — for which the company had lobbied hard.

The public face of its lobbying effort, which included a tax proposal of its own, was FedEx’s founder and chief executive, Frederick Smith, who repeatedly took to the airwaves to champion the power of tax cuts. “If you make the United States a better place to invest, there is no question in my mind that we would see a renaissance of capital investment,” he said on an August 2017 radio show hosted by Larry Kudlow, who is now chairman of the National Economic Council.

Four months later, President Donald Trump signed into law the $1.5 trillion tax cut that became his signature legislative achievement. FedEx reaped big savings, bringing its effective tax rate to less than zero in fiscal year 2018 from 34% in fiscal year 2017, meaning that, overall, the government technically owed it money. But it did not increase investment in new equipment and other assets in the fiscal year that followed as Smith said businesses like his would.

Nearly two years after the tax law passed, the windfall to corporations like FedEx is becoming clear. A New York Times analysis of data compiled by Capital IQ shows no statistically meaningful relationship between the size of the tax cut that companies and industries received and the investments they made. If anything, the companies that received the biggest tax cuts increased their capital investment by less, on average, than companies that got smaller cuts.

FedEx’s financial filings show that the law has so far saved it at least $1.6 billion. Its financial filings show it owed no taxes in the 2018 fiscal year overall. Company officials said FedEx paid $2 billion in total federal income taxes over the past 10 years.

A FedEx truck drives around workers sorting packages on the Upper East Side of Manhattan, Aug. 28, 2019. (Brittainy Newman/The New York Times)

As for capital investments, the company spent less in the 2018 fiscal year than it had projected in December 2017, before the tax law passed. It spent even less in 2019. Much of its savings has gone to reward shareholders: FedEx spent more than $2 billion on stock buybacks and dividend increases in the 2019 fiscal year, up from $1.6 billion in 2018, and more than double the amount the company spent on buybacks and dividends in fiscal year 2017.

A spokesman said it was unfair to judge the effect of the tax cuts on investment by looking at year-to-year changes in the company’s capital spending plans.

“FedEx invested billions in capital items eligible for accelerated depreciation and made large contributions to our employee pension plans,” the company said in a statement. “These factors have temporarily lowered our federal income tax, which was the law’s intention to help grow GDP, create jobs and increase wages.”

FedEx’s use of its tax savings is representative of corporate America. Companies have already saved upward of $100 billion more on their taxes than analysts predicted when the law was passed. Companies that make up the S&P 500 index had an average effective tax rate of 18.1% in 2018, down from 25.9% in 2016, according to an analysis of securities filings. More than 200 of those companies saw their effective tax rates fall by 10 points or more. Nearly three dozen, including FedEx, saw their tax rates fall to zero or reported that tax authorities owed them money.

From the first quarter of 2018, when the law fully took effect, companies have spent nearly three times as much on additional dividends and stock buybacks, which boost a company’s stock price and market value, than on increased investment.

The law cut the corporate rate to 21% from 35% and allowed companies to deduct the full cost of new equipment investments in the year that they make them. Those cuts stimulated the U.S. economy in 2018, helping to push economic growth to 2.5% for the year and fueling a boost in hiring. Business investment rose at an 8.8% rate in the first quarter of 2018 and was nearly as strong in the second quarter.

But the impact dwindled quickly.

In the summer, the economy grew at just 1.9% and business investment fell 3%, including a 15.3% plunge in spending on factories and offices. Over the spring, companies spent less on new investments, after adjusting for inflation, than they had in the winter.

Overall business investment during Trump’s tenure has now grown more slowly since the tax cuts were passed than before.

Some conservative economists and business leaders said the effects of the tax cuts were undercut by uncertainty from Trump’s trade war, which is slowing global growth and prompting companies to freeze projects. Other economists said the fizzle is predictable because high tax rates were not holding back investment.

“It did provide a short-term boost, but it wasn’t the big response that many people expected,” said Aparna Mathur, an economist at the conservative American Enterprise Institute, who recently concluded that the 2017 law has not meaningfully changed investment patterns in the U.S.

Smith, 75, a former Marine who built FedEx from a small package delivery service into a global logistics giant, was no stranger to pressing for lower taxes. He tried, without success, to get President Barack Obama to cut the corporate rate. But with Trump’s ascension, the corporate chief began a one-man campaign to convince Washington that now was the moment. He met with the president-elect at Trump Tower on Nov. 17, just days after the election, and appeared alongside the president at official events.

In a conference call with analysts the month after Trump’s election, Alan Graf, FedEx’s chief financial officer, called the prospect of a 20% corporate tax rate “a mighty fine Christmas gift.”

Smith teamed up with his competitor, David Abney, chairman and chief executive of UPS, to push for a tax overhaul, including jointly writing an op-ed in The Wall Street Journal.

“Fred and I even jointly had some meetings about this with key people, and we were both pushing pretty hard,” Abney said in a recent interview.

FedEx spent $10 million on lobbying in 2017, in line with previous spending, with much of it focused on tax issues, according to federal records. Its team pushed hard to shape the bill behind the scenes, meeting regularly with House and Senate committee staff who were writing the provisions.

Smith met with Trump and Vice President Mike Pence in February 2017, and on May 26 he spoke on the phone with Steven Mnuchin, the Treasury secretary, according to Mnuchin’s public calendar.

Eight months after Congress passed the law, Trump celebrated the tax cuts by hosting Smith and other business leaders at a dinner at his Bedminster, New Jersey, golf club. He singled out Smith several times, bantering with him about a term paper that Smith had written while a student at Yale. The paper formed the basis for the creation of FedEx.

The next week, Smith boasted of his company’s influence on the law in the company’s annual report, which noted that FedEx is “investing more than $4.2 billion in our people and our network as a result of the tax act.”

FedEx increased the size of its workforce by around 4% in its 2018 fiscal year and around 7% in its 2019 fiscal year.

The company also accelerated a previously scheduled wage increase for hourly employees by six months. It gave performance-based pay to other managers and said it would invest $1.5 billion over seven years in its Indianapolis shipping hub. The company also bought 24 Boeing freight jets for $6.6 billion, a purchase officials say would not have happened without tax cuts.

But the company ended its 2018 fiscal year having spent $240 million less on capital investments than it predicted it would in December 2017, shortly before the tax cuts passed. The company’s capital spending declined by nearly $175 million in fiscal 2019.

This year, the company cut back employee bonuses and has offered buyouts in an effort to reduce labor costs in the face of slowing global growth. The company has also added to its pension fund, a move that carried the benefit of reducing its tax liability even further.

FedEx reduced its tax liability in part by taking advantage of a provision in the law that allowed companies to immediately deduct the value of any capital investments they make in a given year. But its biggest gains were from the cut in the corporate rate. FedEx had been carrying a large amount of future tax liabilities on its balance sheet — and when the corporate rate fell to 21%, those liabilities shrank, too.

“Something like $1.5 billion in future taxes that they had promised to pay just vanished,” said Matthew Gardner, an analyst at the liberal Institute on Taxation and Economic Policy in Washington. “The obvious question is whether you can draw any line, any connection between the tax breaks they’re getting, ostensibly designed to encourage capital expenditures, and what they’re actually doing. And it’s just impossible to know.”

This article originally appeared in The New York Times.

© 2019 The New York Times Company |

|

|

|

Post by the Scribe on Apr 8, 2020 23:42:50 GMT

Every Liberal and Democrat said THIS IS WHAT WAS GOING TO HAPPEN IF THE CONSERVATIVES pass their Tax Reform Act for the 1% and corporations. That is exactly what happened again. Bush II pulled the same nonsense with his rich compassionate conservatives and Reagan did it with his ridiculous Trickle Down Economics which in truth is TRICKLE UP ECONOMICS. Corporations don’t operate for the public good. They operate for the benefit of the shareholders and those shareholders are typically wealthy and mostly the 1%. They don't pay income tax because they derive their $$$ mostly through capital gains, real estate, and other money laundering schemes. Ever notice how the mantra from the conservative cons is LOWER THE CAPITAL GAINS TAX? Now you know why. When will the ignorant half of America wake up to what these CONS are pulling? And when will the LEFT get a backbone and STOP this nonsense? VOTE SANDERS OR WARREN. It is the ONLY way things will change to benefit the common workers and middle class in general. And DON'T listen to the fear mongering tactics of the corporate mainstream media, the wealthy, Wall Streeters, politicians who shill for the 1% who will do ANYTHING to prevent the drastic changes we need to happen and all the fools who buy into it.

SEC Commissioner Wants To Pump The Brakes On Corporate Stock Buybacks 46:38 play dts.podtrac.com/redirect.mp3/traffic.megaphone.fm/BUR3121145735.mp3

November 18, 2019

Meghna ChakrabartiWes Martin www.wbur.org/onpoint/2019/11/18/corporations-stock-buybacks-sec-robert-jackson

Securities and Exchange Commission (SEC) Commissioner Robert Jackson Jr., right, during a House Financial Services Committee hearing, Tuesday Sept. 24, 2019, on Capitol Hill in Washington. (Jacquelyn Martin/AP)

SEC Commissioner Robert Jackson says U.S. corporations aren’t helping build the economy. They’re using tax cuts to buy back their own stocks.

He wants to put the brakes on the common corporate practice.

Interview Highlights

On the recurrence, time and time again, of stock buybacks after corporate tax cuts

“We have been to the movie of tax cuts and buybacks before, in the Republican administration during the George W. Bush era. We enacted a quite substantial tax cut during that period. And studies after that showed very clearly that most corporations use the funds from that tax cut for buybacks. And here's the kicker. That particular tax cut actually required that companies deploy the capital for capital expenditures, wage increases and investments in their people. Yet studies showed that, in fact, the companies use them for buybacks. So we've been to this movie before. And what you're describing to me, that corporations turned around and took the Trump tax cut and didn't use it in investing in their people or in infrastructure, but instead for other purposes, shouldn't surprise anybody at all.”

“In my experience, and you know, before I was an FCC commissioner, I was a corporate lawyer. And before then I was an investment banker. My experience is that people do what they're paid to do. People follow their incentives. And the truth is that CEOs don't get paid for making investments in people. CEOs don't get paid for building long term capital investments in American communities. CEOs get paid on the basis of stock price. And so it's not surprising to me at all, as someone who studies incentives, that what they did with the money we gave them was maximize that stock price. Now we can talk as a society about whether or not that's the right thing for them to maximize. And we should. But we ought to be honest with ourselves about what's going to happen when we cut taxes for American corporations, because we've been to this movie before.”

What is the reasoning, on paper, for a corporate buyback of stock?

“The basic law and finance of a buyback works like this. The company has excess capital and has to determine what to do with it. And it will often choose — depending on the projects that are available to it — to return some of that capital to investors, by announcing that the company will buy back shares. And typically the signal that's being sent there is that the company believes that the stock is undervalued. And that as a consequence, they're prepared to use Treasury money at the corporation to buy those shares back.”

If performance in share price is tied to a CEO's compensation, is there perhaps a perverse incentive there?

“Absolutely. So two things to say, and I think you're right, we should unpack these two things. One is the CEO has to decide whether and when to do a buyback. And second, the CEO is paid based on the stock price and indeed paid in shares of stock. And what the CEO would like to do is find a moment in which to sell those shares. And what's really troubling for me is that at the same moment, the company says, ‘The stock is so cheap, we are going to use Treasury money to buy it.’ That's the same moment the CEO says, ‘This is a time for me to sell it.’ And my experience with CEOs is that they don't sell expensive things cheaply. And that's why I'm so troubled by the notion that at the same time they're buying back stock, they're selling their own personal shares.”

From The Reading List

Wall Street Journal: "Tax Cuts Provide Limited Boost to Workers’ Wages" — "U.S. companies are putting savings from the corporate tax cut to use, but only a fraction of it is flowing to employees’ wallets, new data show. www.wsj.com/articles/tax-cuts-provide-limited-boost-to-workers-wages-1538472600

"In the months after the December tax-code overhaul that lowered the corporate rate to 21% from 35%, dozens of companies such as Walmart Inc. and FedEx Corp. announced one-time bonuses and wage increases for hourly workers. Those moves earned praise from the Trump administration as evidence the cuts were quickly reaching many Americans.

"Now, various surveys indicate that most companies aren’t passing the money directly to employees."

CNBC: "Stock buybacks hit a record $1.1 trillion, and the year’s not over" — "It’s official: This is an all-time record year for corporate stock buybacks. www.cnbc.com/2018/12/18/stock-buybacks-hit-a-record-1point1-trillion-and-the-years-not-over.html

"Announced buybacks for 2018 are now at $1.1 trillion. And companies are using their authorizations. About $800 billion of stock has already been bought back, leaving about $300 billion yet to be purchased. We’ve seen buyback announcements recently from Lowe’s, Pfizer, and Facebook, but in the last few days, as stocks have moved to new lows, companies are picking up the pace of activity."

Harvard Business Review: "Are Buybacks Really Shortchanging Investment?" — "It’s no secret that the American economy is suffering from the twin ills of slow growth and rising income inequality. Many lay the blame at the doors of America’s largest public corporations. The charge: These firms prefer to distribute cash generated from their businesses to shareholders through stock buybacks and dividends rather than invest for the long term, undermining job growth and putting our economic future at risk. Excessive distributions to shareholders, it’s further claimed, also increase inequality: They cause wages to stagnate while enriching shareholders and executives. hbr.org/2018/03/are-buybacks-really-shortchanging-investment

"Buybacks in particular have attracted the ire of corporate America’s critics. Larry Fink, CEO of the investment management firm BlackRock, for example, warned corporate leaders against seeking to 'deliver immediate returns to shareholders, such as buy-backs…while underinvesting in innovation, skilled workforces or essential capital expenditures necessary to sustain long-term growth.' Former U.S. Vice President Joseph Biden recently claimed that the high level of buybacks 'has led to significant decline in business investment' with 'most of the harm…borne by workers.' Critics often point to the high ratio of shareholder payouts to net income. As William Lazonick of the University of Massachusetts noted in these pages, stock repurchases and dividends totaled 91% of net income in S&P 500 firms from 2003 to 2012."

Vox: "How did American CEOs get so rich?" — "On October 24, 1929, the American stock market crashed. Fortunes disappeared overnight, and the value of American companies tanked. But the people in charge of those companies had an idea: They started buying shares of their own stock from investors, which meant there were fewer stocks out there for other people to buy. And when there’s less of something, the price goes up. www.vox.com/videos/2019/10/11/20909869/ceo-pay-stock-buybacks

"Corporations had figured out a kind of magic trick. They could jack up their stock price without actually doing anything. This was the beginning of the stock buyback."

This program aired on November 18, 2019.

Related:

Latest Trend: U.S. Companies Are Engaged In Stock Buybacks

From Amazon To Walmart, 2020 Candidates Take On Big Corporations By Name

Meghna Chakrabarti Host, On Point

Meghna Chakrabarti is the host of On Point. |

|

|

|

Post by the Scribe on Apr 8, 2020 23:43:31 GMT

9 Stats That Show the Tax Code Favors the Ultra-RichWithout dramatic tax reform, inequality will continue to skyrocket.

BY IZII CARTER

inthesetimes.com/article/22098/tax-injustice-income-rich-top-earners-tax-rate-saez-zucman-sanders-warren

Economic inequality in the United States is the highest it’s been in the last 50 years. In recent decades, the richest 1% of Americans have accumulated nearly 40% of the country’s wealth. The net worth of just three individuals—Jeff Bezos, Bill Gates and Warren Buffett—dwarfs that of the entire bottom 50% of Americans. And it only seems to be getting worse.

How did we get here? In a new book The Triumph of Injustice: How the Rich Dodge Taxes and How to Make Them Pay, authors Emmanuel Saez and Gabriel Zucman suggest the answer has much to do with changes to the tax code that have reduced the burden of taxation on America’s wealthiest groups and made it easier than ever for corporations to evade paying their dues.

Policy proposals from 2020 hopefuls like Elizabeth Warren and Bernie Sanders are seeking to change that. Warren’s “Ultra-Millionaire Tax” would impose a 2% tax rate on net worth in excess of $50 million, which becomes a 3% tax rate beyond $1 billion. In other words, any wealth between $50 million and $1 billion would be taxed at 2%, but the 1,000,000,001st dollar (as well as anything beyond that) would be taxed at 3%. Sanders’ “Tax on Extreme Wealth” plan goes even further by instituting a 1% tax rate on net worth above $32 million that rises steadily to 8% on all wealth over $10 billion. Warren’s campaign claims her plan would bring in $2.75 trillion in revenue. Sanders’ would likely raise even more, which he proposes to use as funding for his affordable housing plan, universal childcare, and some of Medicare for All.

Here are nine statistics from The Triumph of Injustice that show how tax injustice has contributed to inequality in America and the urgent need for reform:

52% — U.S. corporate tax rate in 1952

21% — U.S. corporate tax rate after Trump’s tax law

0% — Corporate tax rate in Bermuda

60% — Portion of profits U.S. multinationals collectively book in low-tax countries like Bermuda and Ireland

$25,000 — FDR’s proposed “maximum income” in 1942 (about $400,000 today), above which income would be taxed 100%

$1,500,000 — Average income of the top 1% of American earners today

37% — Current top marginal tax rate in America, 20% below the historical average

2018 — First year in history that America’s top 400 richest individuals paid less in taxes than the bottom 50% of earners

25% — Fraction of unpaid taxes owed by the ultra-rich, almost 15% more than for other income levels |

|

|

|

Post by the Scribe on Apr 8, 2020 23:44:08 GMT

If you didn't get screwed enough from the Republicon Tax Reform Act from last year....GET READY....they are coming after you again to get the rest.New W-4: Adjusting your tax withholdings just changedYahoo Money Janna Herron

Editor

Yahoo Money December 8, 2019

money.yahoo.com/new-tax-form-w4-161555144.html?re=0&.tsrc=notification-brknews

Adjusting how much tax is withheld from your paycheck will likely now take longer — except for working married couples — thanks to a new Form W-4 released this week from the Internal Revenue Service.

The new form is longer and gets rid of allowances that you could claim for yourself and other family members. Instead, it asks for more precise information that may require a second look at last year’s taxes. The changes to the form better reflect the President Trump-backed tax law that went into effect in 2018.

Generally, it’s important to get withholdings right. If too little is withheld, you end up owing the IRS.

For the most part, if a worker’s tax status hasn't changed from last year, they don’t need to fill out a new W-4. New employees and those who experienced a major life event like getting married or having a child need to submit a new one. Also, if you’re unhappy with your 2019 tax outcome – say, you get a smaller refund or owe money to Uncle Sam – you should also complete a new W-4.

The form is actually simpler than the one it replaced, Pete Isberg, vice president of government affairs at the payroll company ADP, told Yahoo Finance. But it will take more time for people to fill out.

“It used to be a 30-second exercise,” Isberg said. “I expect now many folks will have to dial home and ask someone to look up last year’s tax returns.”

The Internal Revenue Service released a new Form W-4 to help taxpayers accurately adjust their paycheck withholdings. (Source: IRS)

More

Better for married couples

The new form should be “vastly easier” for married couples who both work, Isberg said, as long as they follow the instructions.

Gone is the messy and difficult nine-step worksheet to figure out how much each couple should withhold from their individual paychecks. Now, married working couples only need to check a box to indicate that they both have jobs and the correct withholdings will be calculated for them.

However, potential tricky part comes in Steps 3 and 4. If a couple checks the working box, only the highest-earning spouse should fill out Steps 3 and 4, which ask for dependents, additional income, deductions, and extra withholdings.

If you and your spouse both fill out the extra income in Step 4, then too much will be withheld from your paychecks. If you both fill in deductions or dependents, too little will be withheld and you could end up with a big tax bill.

Serious African American couple discussing paper documents, sitting together on couch at home, man and woman checking bills, bank account balance, terms of contract, mortgage, loan agreement

The new Form W-4 should be easier for working married couples to fill out than the previous version.

Be prepared

The best way to fill out the new form properly is to have last year’s total deductions, other income, and tax credits for dependents handy. Isberg encourages employers to allow new workers to take the form home, rather than expecting it done on their first day.

The key thing, Isberg said, is to take your time and read the instructions.

“Nobody wants a surprise,” he noted.

Janna is an editor for Yahoo Finance. Follow her on Twitter @jannaherron.COMMENTSKevinjay4 hours ago

I am a tax pro... the entire tax cut package was/is a money grab for the rich and corporations. It specifically hurts middle income, union workers, and large families. Good job GOP. And it doe not provide an alternative source of tax revenue, like taxing corporate share buybacks, or excess health insurance profits.

Mickey4 hours ago

I'm considered low income and my federal taxes went up considerably last year. Where's the tax cut for the middle and low? All we get is lower income.

steve4 hours ago

One thing I know for sure whenever there is something done to the tax code it will not favor the working man

Lou4 hours ago

Thanks for the increase in taxes and time it takes to file. But the top 1% gets a big easy tax break.

Lots wrong with this picture

Doug5 hours ago

Are we getting a REAL middle class tax cut? If you don't make millions or billions, the answer is an unequivocal, NO.

adouglass7924 hours ago

Why do a married couple pay less in taxes than single filers? They have 2 incomes. Where’s the logic?

maria b5 hours ago

So, trump gives a huge tax break to corporations and everyone else has to account for everything. The transparency of his taxes though, not so much.

Amber4 hours ago

Life is just plain hard right now. I own and run a real estate business with my mom and sister. We have experienced our worst year in the 10 our doors have been open. We have so little money that a closing next week has to happen otherwise none of us get paid. I have rent and a $960 bankruptcy payment to make every month along side all the regular bills and taking care of my 12 year old daughter's needs. I'm a single mom. Nothing seems to be getting easier for anyone except the wealthy. Trump doesn't care about anyone except the big wigs that line his pockets in exchange for him lining theirs. Meanwhile, the rest of us are working ourselves into poverty no matter how hard we try not to. What happened to this country?

UNAVAILABLE4 hours ago

Last year I paid more in taxes because I was unable to deduct my state and local taxes. I own a lot of property and a large portion of my income goes to property tax. My accountant told me it was going to get worse. Our deductions are being eliminated more and more each year. Looks like he was right.

CJ4 hours ago

I work 48-60 hours a week just to pay my bills, and that's without kids or a wife. I have no idea how people with kids can afford anything.

TAX$USONLY5 hours ago

thinkprogress.org/10-million-american-families-saw-tax-increases-under-trump-tax-cut-aa97d7aee410/

Billy4 hours ago

Trump gives a tax cut and also increases the standard deduction. That's great for someone who lives in an apartment and doesn't have 8- 10k in mortgage interest a year. But the middle class homeowner who has the additional expense of maintaining a home gets no more benefit then a renter. Writing off mortgage interest was just one of the benefits of owning a home. Doesn't matter now, thanks to Trump.

BL3 hours ago

People should not have been given a new, lower tax on their paychecks. It put a lot of people in debt to the IRS. Many people actually believe what trump says so when he gives instructions to the IRS to give a low tax rate on their paychecks then what they actually should have been, like last year, it isn't their fault they owe taxes, it's our lying president's fault for telling the IRS to change the rates on payroll taxes to make it look like they got a tax cut.

John4 hours ago

As long as were talking about Taxes Trump promised before election to release his, Hows that coming along ?

True Republicans R Gone3 hours ago

Trump is driving this because all his borrowing and tax cuts need to be paid for. The great experiment in trickle down is a flop (revenue is down) and consumer goods cost far more than when he stepped into office. The middle class exists on salaries... so it's an easy way to latch onto the money... eliminating the strategy many of us have had in saving money we would normally pay in taxes until the taxes are due - giving us some money (not discretionary) for a while. It's actually more "big brother" stuff. And guess who still gets over? Those corporations who defer what they owe until tax time. It's a scam.

frank4 hours ago

There should be no fed tax on anyone making less than 40k, and 80k for married couples. Let the billionaires make up the difference

jeffyesterday

@pittbull Your remark is very ignorant but not surprising since your a Trump ### kisser and worship him as a God. Did you read the comment? Why would you think the person is lying? You don't think that people that work full time and after they pay all the bills, have very little left over to do any thing. Why would you make such an ignorant statement that they are from the left or a Liberal. People that are a Conservative are in the same boat. They may not want to admit it or talk about it because they worship Trump, but they don't have any more money left over than a Liberal does. Maybe you should stop listening to only Fox news and hateful people like Sean Hannity and anarchists like Mark Levin, because that's all they do is make a Democrat or Liberal the Boogie Man because they want higher television ratings or to sell more books. My advice to you is to start thinking for yourself because you may not realize it, but your comments make you sound like an ignorant brainwashed moron.

webyesterday

What happened to the 10% tax cut for the middle class that Trump promised for November of 2018? Trump have TRILLIONS to his richest friends while taxes and health care costs for the middle class have rose to the highest levels in history. When are some of you middle class tax payers going to learn that Donald Trump and the Republicans have been picking your pockets for years and years?

James Cyesterday

Every year my divorce I was able to claim the alimony I gave my ex wife as she had to claim that income in her tax return. Now I don't have that luxury any more that TRUMP has basically given this deduction to the millionaires. Thanks TRUMP for making my taxes and the IRS get more of my money each year. THANKS AGAIN TRUMP for making my taxes simple.

Timyesterday

The top 1 percent will pay less but the real winners will be the top 1 percent of the top 1 percent (like trump and his family and family).

Richardyesterday

2018 was the first year the wealthiest people paid less taxes than the working middle class

www.google.com/amp/s/amp.businessinsider.com/american-billionaires-paid-less-taxes-than-working-class-wealth-gap-2019-10

Williamyesterday

We got it done! I am (was) middle class and my taxes went up by $20,000 in 2017 and 2018 on the same income. Undo it you rich Republican crooks. You have effectively wiped out the middle class. The only reason that you can say there is still a significant middle class is that most people work in excess of 60 hours per week and that's not even counting the spouse. Years ago, a single full time job income would sustain a family. Those days are long gone. Automation should have resulted in less weekly work hours but that is not the case. People work more hours for less "real income"in order to make the rich 1% richer. It's amazing how the Trumptards still swallow his Fox News Kool Aid like lemming being led over the cliff.

Jackieyesterday

coming from a man who ''HIDES'' his taxes...gives his '#$%$ a ''HUGE'' uncontested gift of a lifetime supported by the ''ENTIRE'' REPUBLICAN PARTY..while the struggling ''MIDDLE'' CLASS who's ''BONUS'' so to speak is only ''TEMPORARILY'' if $10.00 -$12.00 bucks extra on their pay checks will soon be coming to an end then what???

Chaiyesterday

The only surprise I get is how much tax I have to pay and yet realize that my CEO's pay nearly nothing. Thanks GOP, you guys are the best.......at serving yourselves.

|

|

|

|

Post by the Scribe on Apr 8, 2020 23:44:47 GMT

Trump tax ‘cut’ actually increased taxes for 10 million American families, report findsA Center for American Progress estimate found that 10,260,263 families saw their taxes go up, thanks to the 2017 law.

JOSH ISRAEL

APR 12, 2019, 12:48 PM thinkprogress.org/10-million-american-families-saw-tax-increases-under-trump-tax-cut-aa97d7aee410/

PRESIDENT DONALD TRUMP HELD AN EVENT IN JUNE CELEBRATING THE SIX-MONTH ANNIVERSARY OF HIS TAX BILL. CREDIT: CHERISS MAY/NURPHOTO VIA GETTY IMAGES

Donald Trump ran in 2016 promising that every American would receive a tax cut. But he has already raised taxes on an estimated 10 million families, according to a new analysis.

The Center for American Progress released its calculations on Friday, based on data from the non-partisan Institute on Taxation and Economic Policy. It found that 10,260,263 American families saw a tax hike last year, thanks to the president’s 2017 Tax Cut and Jobs Act. (ThinkProgress in an editorially independent news site housed at the Center for American Progress Action Fund.)

“Everybody is getting a tax cut, especially the middle class,” Trump told CNN in May 2016.

As he signed the bill into law in December 2017, he claimed the bill would immediately benefit all Americans. “They’re going to start seeing the results in February. This bill means more take-home pay. It will be an incredible Christmas gift for hard-working Americans,” he bragged. “I said I wanted to have it done before Christmas. We got it done.”

As taxpayers have been filing their 2018 taxes in recent weeks, many have found that they are not getting the refunds they have in the past or even owe the federal government money. The bill’s supporters have dismissed these concerns, suggesting that the higher take home pay thanks to the bill means people were not having as much excessive withholding — a feature, not a flaw.

But these numbers reveal that for millions of Americans, it is not just a misconception; their taxes actually did go up thanks to the law. Much of this had to do with the elimination of personal and dependent exemptions, caps on the State and Local Tax (SALT) deductions, and the termination of the employee business expenses deduction. The SALT deduction cap especially punished families in states like California, Illinois, New Jersey, and New York, which rely on higher revenues and — likely not coincidentally — voted in large numbers for Trump’s opponent in 2016. An estimated 1,736,118 Californians and 1,211,721 New Yorkers saw tax increases, while just 624,481 Texans saw increases.

Steve Wamhoff, who authored the Institute on Taxation and Economic Policy’s study, told ThinkProgress that the 10 million estimate is correct. “Most families did receive a tax cut from the Trump tax law,” he observed. “The real problem is that vast majority of the tax cuts went to people who do not need help. Half the tax cuts went to the richest five percent, which about a quarter going to the richest one percent. Those among the top five percent got bigger tax cuts not just in dollar terms but even when measured as a share of their total income.” |

|

|

|

Post by the Scribe on Apr 8, 2020 23:45:27 GMT

Democrats Take Final Swipe at SALT Cap Before Year’s EndBloombergDecember 10, 2019, 7:38 AM MST

Democrats Take Final Swipe at SALT Cap Before Year’s End

www.yahoo.com/news/democrats-final-swipe-salt-cap-134714001.html

(Bloomberg) -- House Democrats are making a last-ditch bid to reverse the $10,000 cap on state and local tax deductions before year’s end. But they’ll likely need to renew their efforts in 2020 -- or beyond -- because the legislation has no chance of becoming law this year.

Democrats in Congress, governor’s mansions and state legislatures have tried a slew of tactics to repeal the $10,000 SALT cap or find ways around it. Their attempts been stymied by courts, the Treasury Department and Republicans on Capitol Hill.

This time, Democrats are pursuing legislation, released late Monday, that would temporarily raise the SALT cap to $20,000 for married couples in 2019, before repealing it fully in 2020 and 2021.

The cap would revert back to $10,000 in 2022 and would be paid for by raising the top individual tax rate to 39.6% from 37%. The bill also would decrease the income threshold for the highest tax bracket.

The higher rates and new brackets would stay in effect through 2025 when the Republican tax law is scheduled to expire. The SALT deduction and rate changes would raise a net $6.2 billion over a decade, the congressional scorekeeeper, the Joint Committee on Taxation, estimated Tuesday.

“We’re going to do it,” said Representative Bill Pascrell, a New Jersey Democrat who is sponsoring the bill. “You just keep on moving. You don’t back off and surrender and pout.”

The House Ways and Means Committee is scheduled to vote Wednesday on the bill. With the House eyeing a Dec. 20 departure for the year, Democrats leading the effort say they’re seeking a floor vote by the end of 2019.

But the measure will be competing for floor time against several other pressing issues. Lawmakers are finalizing articles of impeachment against President Donald Trump, working to pass spending legislation to avert a government shutdown before the Christmas holiday and potentially considering a revised trade deal between the U.S., Mexico and Canada.

Still, SALT remains a priority for many Democrats who view it as a way to fix one of the most politically contentious portions of the 2017 Republican tax law. Democrats say Republicans targeted residents of high-tax states like New York, New Jersey and California, which are largely represented by Democrats, to pay for their $1.5 trillion corporate and individual tax cut.

The tax break was previously unlimited, with some restrictions if the taxpayer was subject to the alternative minimum tax. Raising the cap for married couples this year and the two-year repeal will mean more people in those high-tax states will see their liabilities decrease temporarily. Republicans have criticized the bill, saying the savings will go to high-income taxpayers who don’t need a tax subsidy.

The tax break is particularly important to moderate Democrats, who represent suburbs outside of Chicago, New York and Los Angeles. Representatives Lauren Underwood of Illinois and Mike Sherrill of New Jersey are among the Democratic freshman who ousted Republican incumbents in the 2018 mid-terms, partially because voters were angry to see their SALT tax break limited.

House passage would likely be the last stop for the legislation, which leaders in the Republican-controlled Senate have said they won’t consider.

That’s a familiar theme in the SALT saga. State legislatures have tried passing laws allowing residents to bypass the $10,000 limit, only to be blocked by the Treasury Department. New York, New Jersey, Connecticut and Maryland sued the Trump administration over the cap, but a judge tossed out the case. The decision is being appealed.

Even lawmakers who want to see the cap raised are pessimistic that the efforts are worth it.

“I don’t see any movement before the end of the year,” said Representative Peter King, a New York Republican who supports raising the cap. “I can’t see Senate Republicans accepting that.“

(Updates with a new fourth paragraph about legislation cost and expiration.)

To contact the reporter on this story: Laura Davison in Washington at ldavison4@bloomberg.net

To contact the editors responsible for this story: Joe Sobczyk at jsobczyk@bloomberg.net, Elizabeth Wasserman, Wendy Benjaminson

For more articles like this, please visit us at bloomberg.com

©2019 Bloomberg L.P |

|

|

|

Post by the Scribe on Apr 8, 2020 23:46:36 GMT

New laws and regulations that could impact your finances in 2020Alexis Keenan Reporter

Yahoo FinanceDecember 13, 2019, 12:53 PM MST

With a new year comes a new set of rules that could bulk up or slim down your 2020 pocketbook.

From adjusted IRS withholding tables that could change take-home pay and help taxpayers avoid costly penalties, to minimum wage increases in 25 states, to amended overtime pay requirements, now is a good time to consider whether the changes could impact your financial goals.

W-4 Withholding

On Dec. 5, the federal government issued a new, more detailed, version of Form W-4, also known as the Employee’s Withholding Allowance Certificate. The update stems from the 2017 Tax Cuts and Jobs Act (TCJA), which among other changes to the Tax Code, altered federal income tax rates and brackets starting in 2018, and in turn, shifted IRS withholding tables.

“This is essentially a delayed reaction to the TCJA that took effect in 2018,” Pete Isberg, vice president of government relations for ADP, said. “Income tax withholding essentially has undergone a very major overhaul for 2020 that could be a source of confusion.” The new form is longer and requires more input from employees, and adds a new filing status option for head of household filers.

The most significant change is that the IRS has done away with the “allowances” method to estimate withholding.

This year will see a change in the way people in the U.S. file their taxes. Source: Getty

“Withholding allowances have been the basis for payroll withholding forever,” Isberg said. “So that's going to cause a little confusion.”

Another change will impact taxpayers with multiple jobs and married filers filing jointly.

“The tax tables just assume that spouses earn about the same amount, and it divides the standard deduction and the tax brackets kind of equally between two jobs,” he said. The new section replaces a 9-step process previously used to estimate withholding for multiple income households.

Also changed is an elective section allowing taxpayers to withhold for separate sources of income, such as interest, dividends, and retirement income.

Taxpayers who have previously submitted a Form W-4 and have not sent in the new version are not required to update or replace their submission. However, penalties for underpayments resulting from outdated form calculations will be assessed for the first time beginning with filings for the 2019 tax year. Those who begin new employment after 2019, or wish to adjust their withholding, must complete the new form.

On its website, the IRS reminds taxpayers to recheck withholding again at the start of 2020. A reassessment is especially important, the agency says, for those taxpayers who reduced withholding in 2019, or did not file a new Form W-4 for 2020. A calculator to estimate withholding is also provided on the agency’s website.

California’s AB5

One of the most sweeping changes for 2020 income earners is estimated to impact at least 1 million of the state’s “gig” economy and freelance workers, reclassifying them from independent contractors to employees. The controversial law mandating the change, State Assembly Bill 5, passed by the state’s legislature in 2019 and effective Jan. 1, 2020, is estimated to cover more than half of the state’s independent contractors. That means employers will be required to provide benefits such as paid sick leave, break time, minimum wage, and work injury compensation, as well as observe their right to unionize.

The law, widely publicized for its debated application to Uber (UBER), Lyft (LYFT), and other ride-hailing drivers currently categorized as independent contractors, is estimated to drive up costs for companies as much as 30%.

A study from the University of California Berkeley determined that under the new law 64% of all California workers whose main employment comes from independent contract work will be required to be reclassified as employees.

A pedestrian walks by Uber headquarters on September 23, 2019 in San Francisco, California. (Photo by Justin Sullivan/Getty Images)

“It’s going to be really difficult to have anybody help you in a practical respect without treating them as an employee, even if they're short term,” Mark Herbert, vice

more www.yahoo.com/news/2020-laws-regulations-personal-finance-195341691.html |

|

|

|

Post by the Scribe on Apr 8, 2020 23:47:13 GMT

'Silicon Six' Paid Even Less In Taxes Than Previously Thought, Watchdog Group Says 05:46Play dts.podtrac.com/redirect.mp3/traffic.megaphone.fm/BUR9049433867.mp3

December 16, 2019

www.wbur.org/hereandnow/2019/12/16/tax-loopholes-silicon-companies

Loopholes allowed six of the biggest Silicon Valley companies to avoid paying about $100 billion in taxes since 2010, according to an analysis by the British group Fair Tax Mark. The group says the corporate tax paid by U.S. tech companies is much lower than commonly understood.

Facebook, Apple, Amazon, Netflix, Google and Microsoft collectively paid $100.2 billion less than they accounted for internally, according to the report, despite having a combined market capitalization of $4.5 trillion.

Here & Now's Tonya Mosley speaks to Paul Monaghan, CEO of Fair Tax Mark.

This segment aired on December 16, 2019. |

|

|

|

Post by the Scribe on Apr 8, 2020 23:47:44 GMT

Republican party a "working class party"....what a laugh. They have the lower class less educated good old boys and their women, some of the evangelicals and most of the conservative, racist and xenophobic rich old white men in their corner as their base now. As the demographics of our country move away from that "base" it will be interesting to see to what lows they will stoop to hold on to their power. Tax revenues paid by Corporations as a fraction of GDP is now one third of what it was in 1960. They are no longer paying their fair share by a long shot. US debt/GDP had been falling from 1945 until 1980 when Reagan started eliminating all the top tax brackets. Since then, wealth disparity has been increasing and GDP growth has been falling. This has all been driven by the GOP and was accelerated by Trump’s tax giveaway.Champion of the middle class? How gullible are people? How Trump has betrayed the working classThe GuardianDecember 22, 2019, 12:47 PM MST

www.yahoo.com/news/trump-wants-champion-working-class-185301179.html

Trump is remaking the Republican party into … what?

For a century the GOP has been bankrolled by big business and Wall Street. Trump wants to keep the money rolling in. His signature tax cut, two years old last Sunday, has helped US corporations score record profits and the stock market reach all-time highs.

To spur even more corporate generosity for the 2020 election, Trump is suggesting more giveaways. Acting chief of staff Mick Mulvaney recently told an assemblage of CEOs that Trump wants to “go beyond” his 2017 tax cut.

Photograph: Nicholas Kamm/AFP via Getty Images

Trump also wants to expand his working-class base. In rallies and countless tweets he claims to be restoring the American working class by holding back immigration and trade.

Most incumbent Republicans and GOP candidates are mimicking Trump’s economic nationalism. As Trump consigliere Stephen Bannon boasted recently: “We’ve turned the Republican party into a working-class party.”

Keeping the GOP the Party of Big Money while making it over into the Party of the Working Class is a tricky maneuver, especially at a time when capital and labor are engaged in the most intense economic contest in more than a century because so much wealth and power are going to the top.

Armed with deductions and loopholes, America’s largest companies paid an average federal tax rate of only 11.3% on their profits last year, roughly half the official rate under the new tax law – the lowest effective corporate tax rate in more than eighty years.

Yet almost nothing has trickled down to ordinary workers. Corporations have used most of their tax savings to buy back their shares, giving the stock market a sugar high. The typical American household remains poorer today than it was before the financial crisis began in 2007.

Trump’s tax cut has also caused the federal budget deficit to balloon. Even as pre-tax corporate profits have reached record highs, corporate tax revenues have dropped about a third under projected levels. This requires more federal dollars for interest on the debt, leaving fewer dollars for public services workers need.

The Trump administration has already announced a $45bn cut in food stamp benefits that would affect an estimated 10,000 families, many at the lower end of the working class. The administration is also proposing to reduce Social Security disability benefits, a potential blow to hundreds of thousands of workers.

The tax cut has also shifted more of the total tax burden to workers. Payroll taxes made up 7.8% of national income last year while corporate taxes made up just 0.9%t, the biggest gap in nearly two decades. All told, taxes on workers were 35% of federal tax revenue in 2018; taxes on corporations, only 9% .